-

Get real-time alerts & clear visibility into the insights that drive decisions.

-

Aggregate data from multiple sources for the context you need.

There's no alpha in busywork. Make success automatic with one integrated workspace that improves efficiency, collaboration, & decision-making at scale.

-

Automate time-consuming manual processes.

-

Use purpose-built productivity tools. Boosted by AI.

-

Connect your talent to knowledge, tools, & data they need.

-

Improve transparency for fast, frictionless reporting.

"VerityRMS is a game-changer. The AI innovations are speeding our workflows.”

Director of Research, The London Company

Why VerityRMS? It's where the world's top firms secure their most valuable asset — their intellectual property — and enrich workflows with best practices & innovation.

The Most Reliable. The Most Innovative.

Research management systems continue to evolve. In a landscape with legacy and lightweight systems, VerityRMS leads the way with tech that helps funds build on best practices while staying a step ahead with the latest innovations.

We Know What Works

VerityRMS is designed for institutional investors — and our products and teams are locked into the needs of direct investors. Verity’s veteran customer success teams have helped the world’s top funds transform how they manage research.

No Pushback From Your Team

An intuitive user experience ensures your firm’s widespread adoption — without losing a step. Robust integrations and configurability let you protect your team’s process from disruption.

Scale Across Asset Classes

Public equity. Private equity. Fixed income. Hybrid approaches. VerityRMS has built-in tools, workflows, and best practices that accommodate modern strategies and areas of focus.

Power Your Continuous Improvement

With easy no-code configuration, dedicated customer support, and a pioneering roadmap, VerityRMS helps your firm quickly adapt to changing demands.

Approved by CTOs & CCOs

With enterprise-grade security and built-in transparency, VerityRMS easily clears your firm’s IT and compliance requirements.

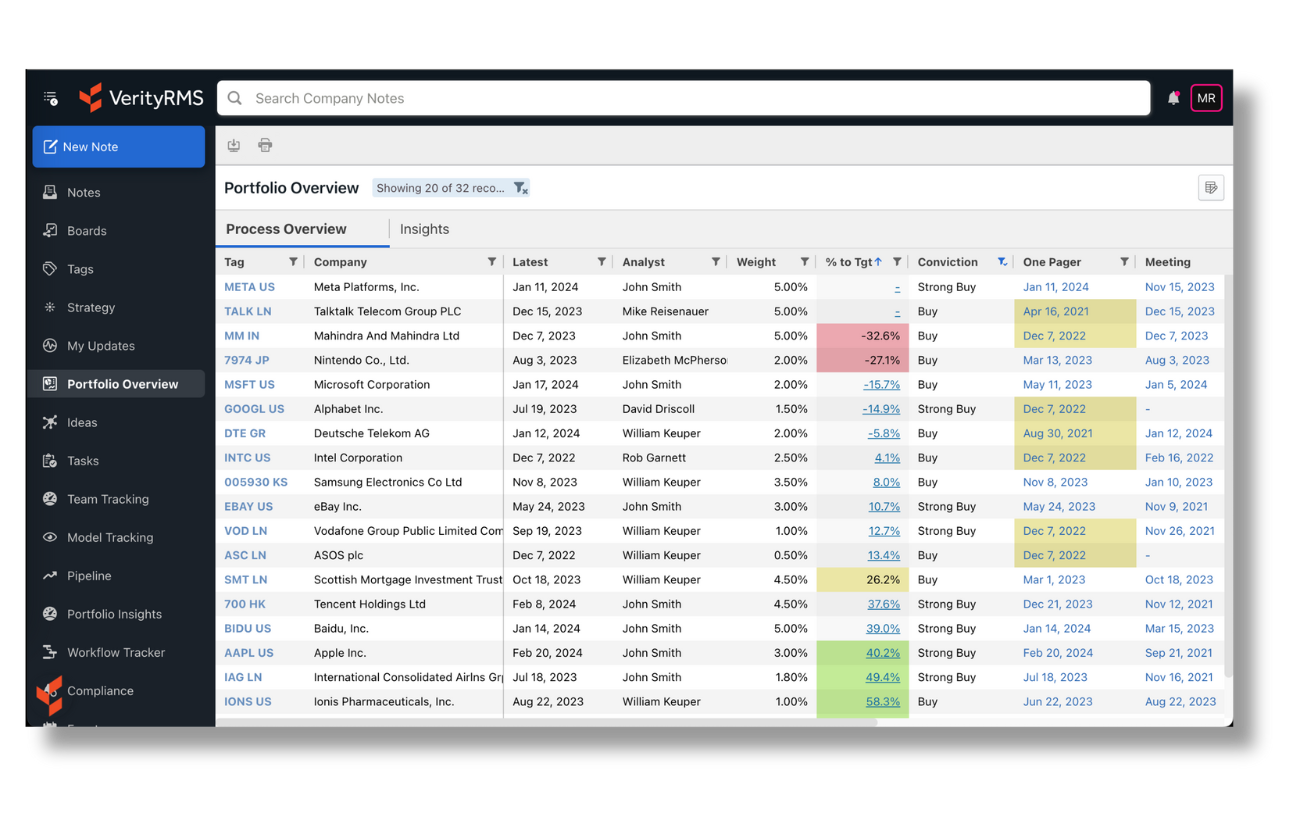

Sample portfolio overview dashboard

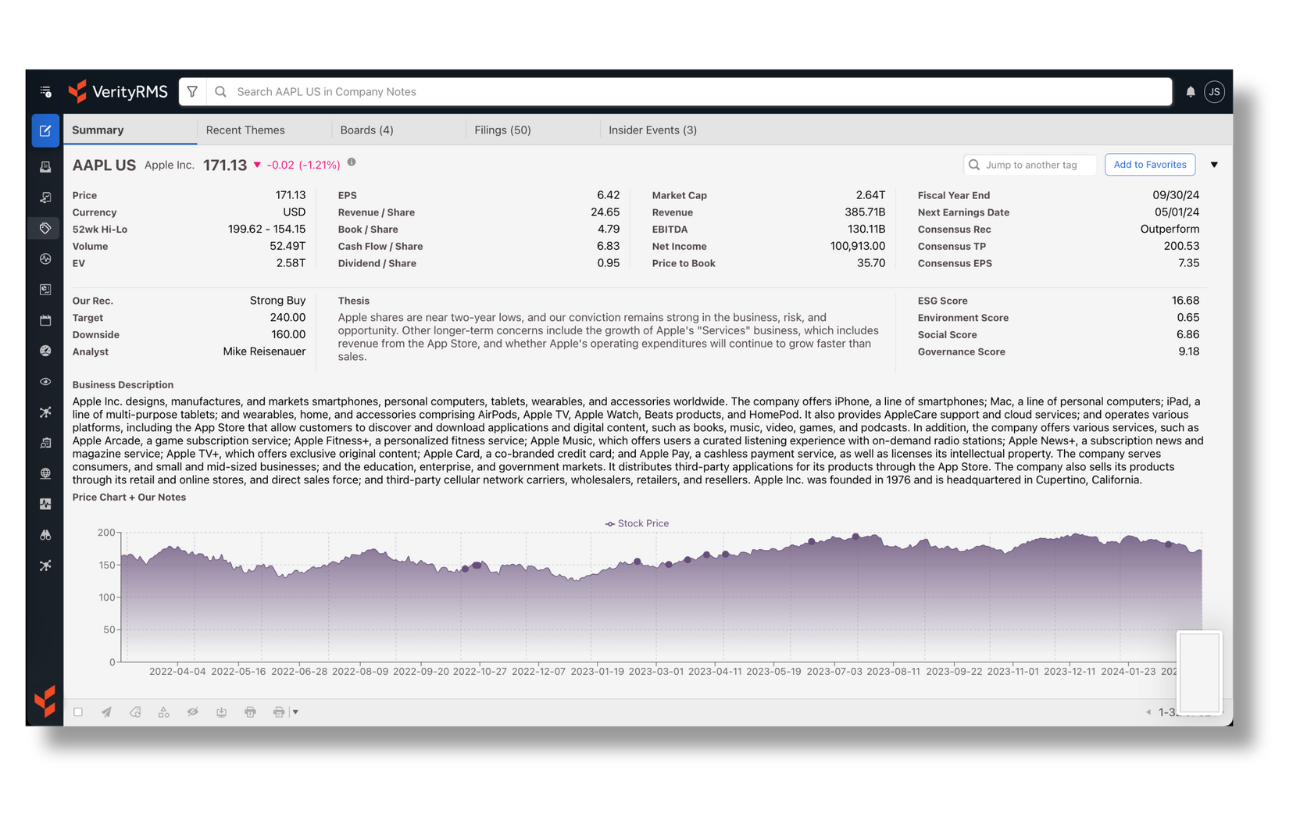

Sample company tearsheet

Get Instant Clarity Across Your Portfolios

Make more informed decisions with the clearest picture of your investment universe. See analyst data alongside third-party data. S&P Global Market Data comes standard.

Features

-

Bespoke dashboards aggregate what matters to you.

-

Customizable tearsheets gather company insights.

-

Data agnostic: you're free to pull in third-party sources.

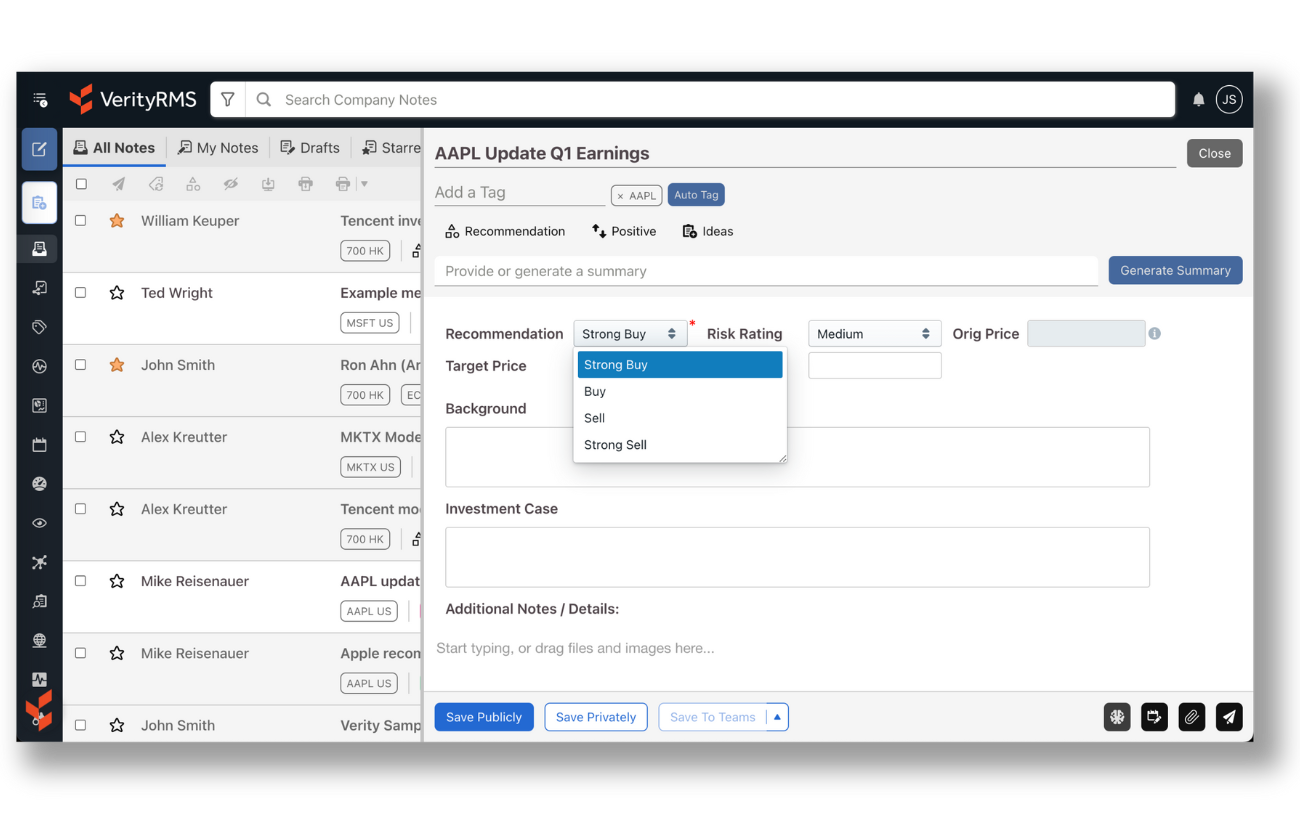

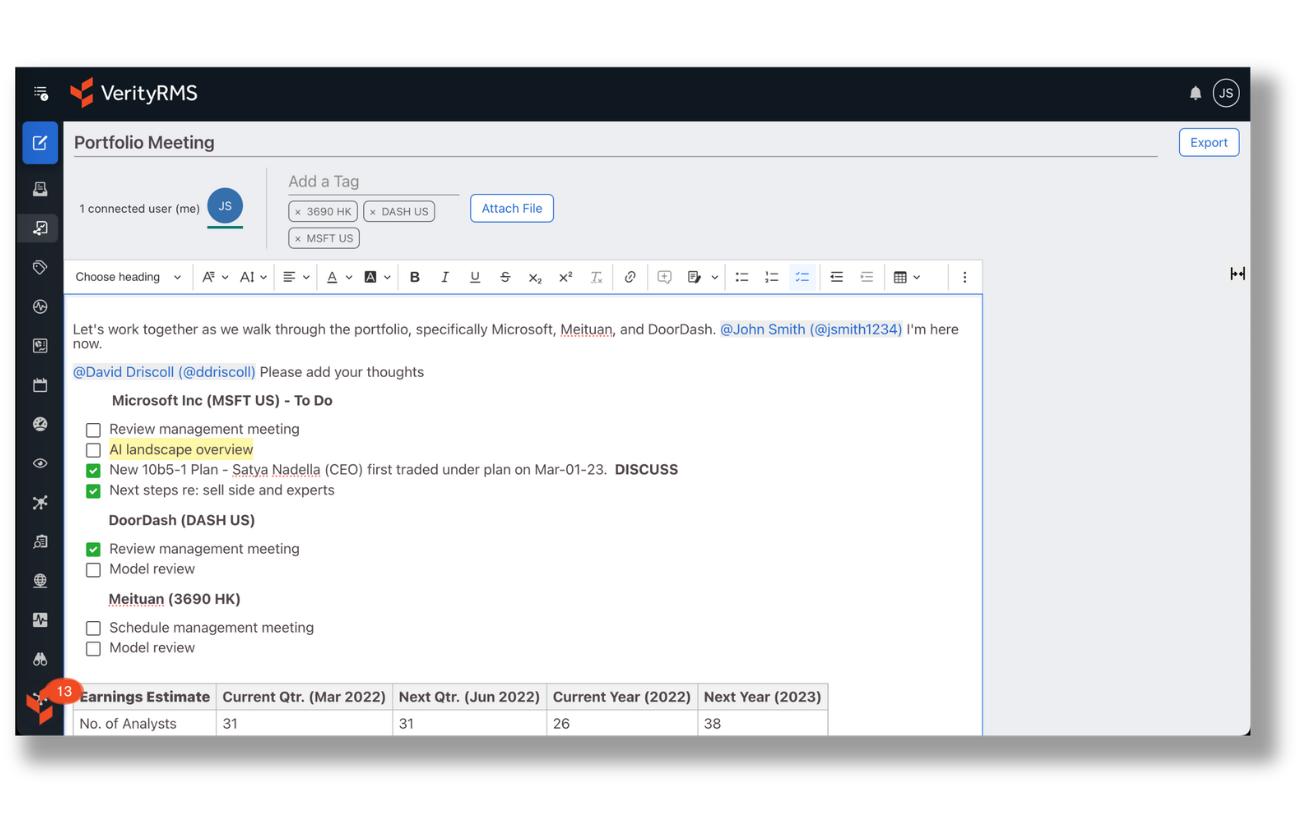

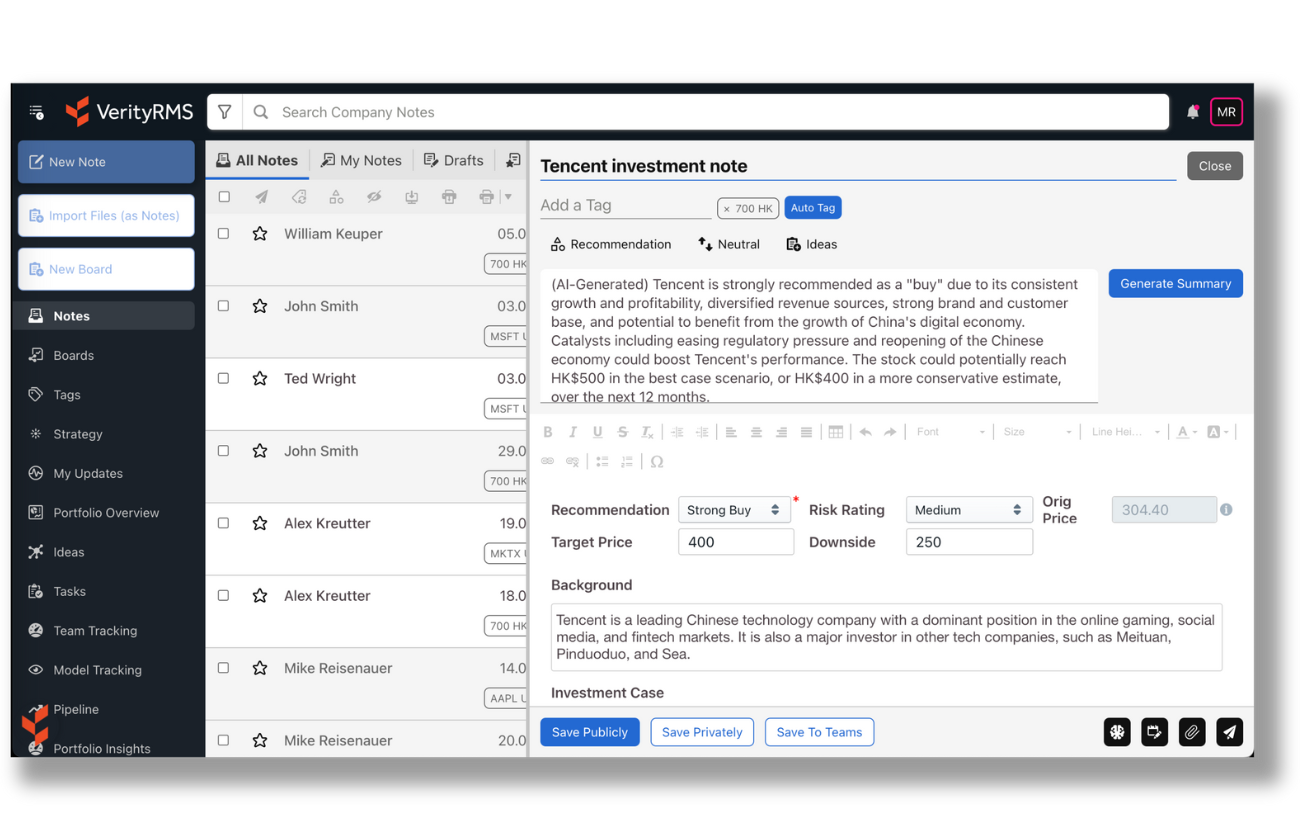

Create & Discover Research Quickly

Easy to use. Easy to master. Analysts create and find research effortlessly.

Features

-

Note experience keeps analysts focused, organized.

-

Powerful search surfaces what you need or forgot.

-

Integrations let analysts author from favorite apps.

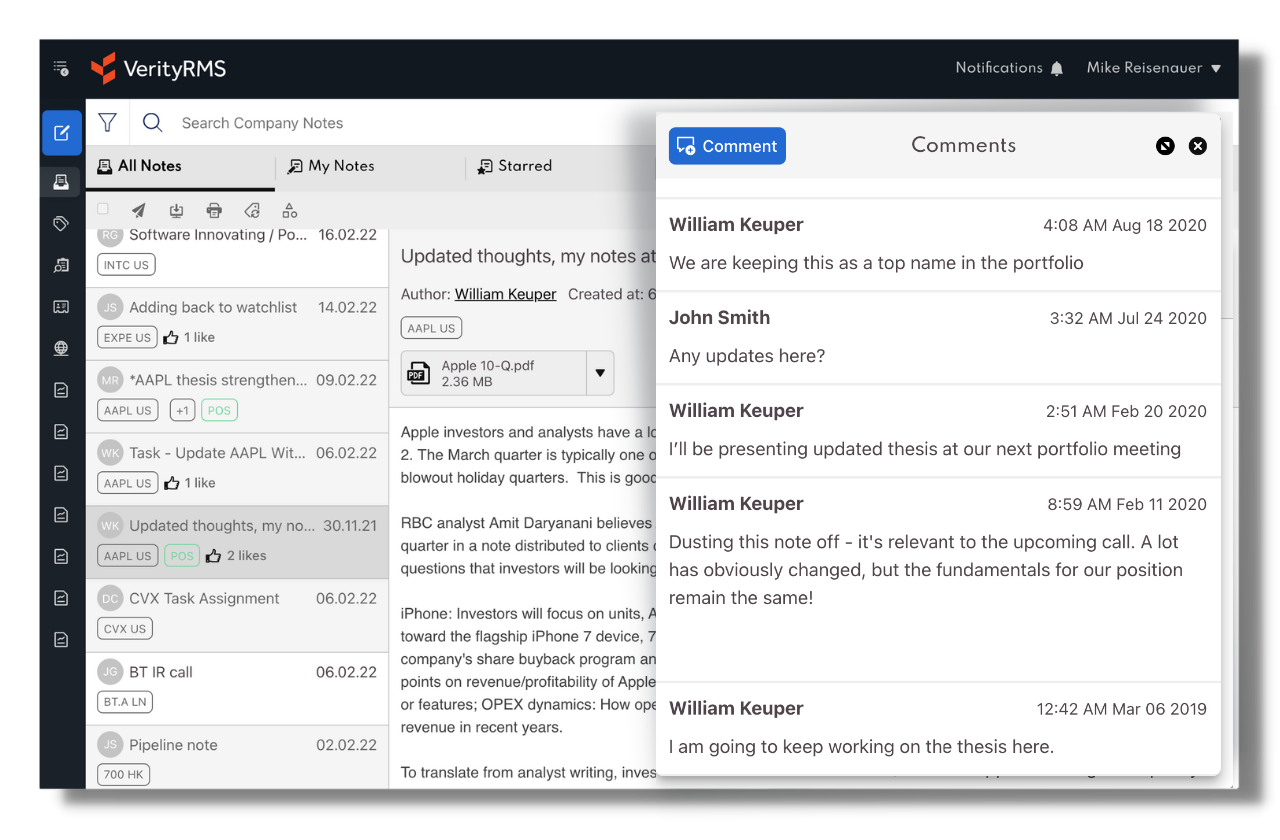

In-app commenting

Live document editing

Collaborate at Scale

Wherever your teams are. Whatever they are working on. It's easy to tackle together.

Features

-

In-app commenting lets team discuss & debate ideas.

-

Shared calendars give cross-team visibility into events.

-

Live document editing spurs real-time collaboration.

-

Native iOS & Android apps keep teams connected.

Automate Reporting — In Real-time

No more spreadsheet hopping or repetitive data entry. Teams get the data they need when they need it. Minimal effort.

Features

-

Flexible data capture enables custom report creation.

-

Compliance capabilities allow one-click reporting.

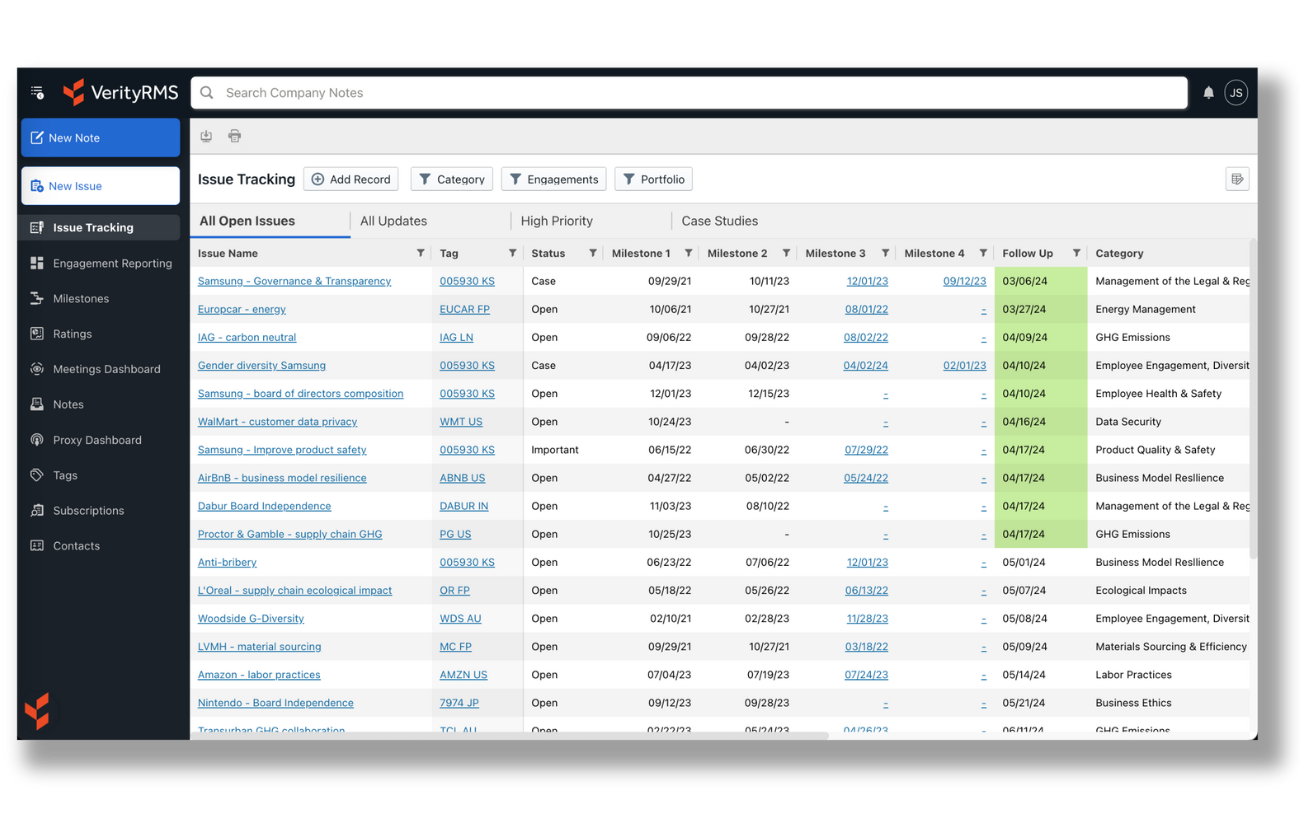

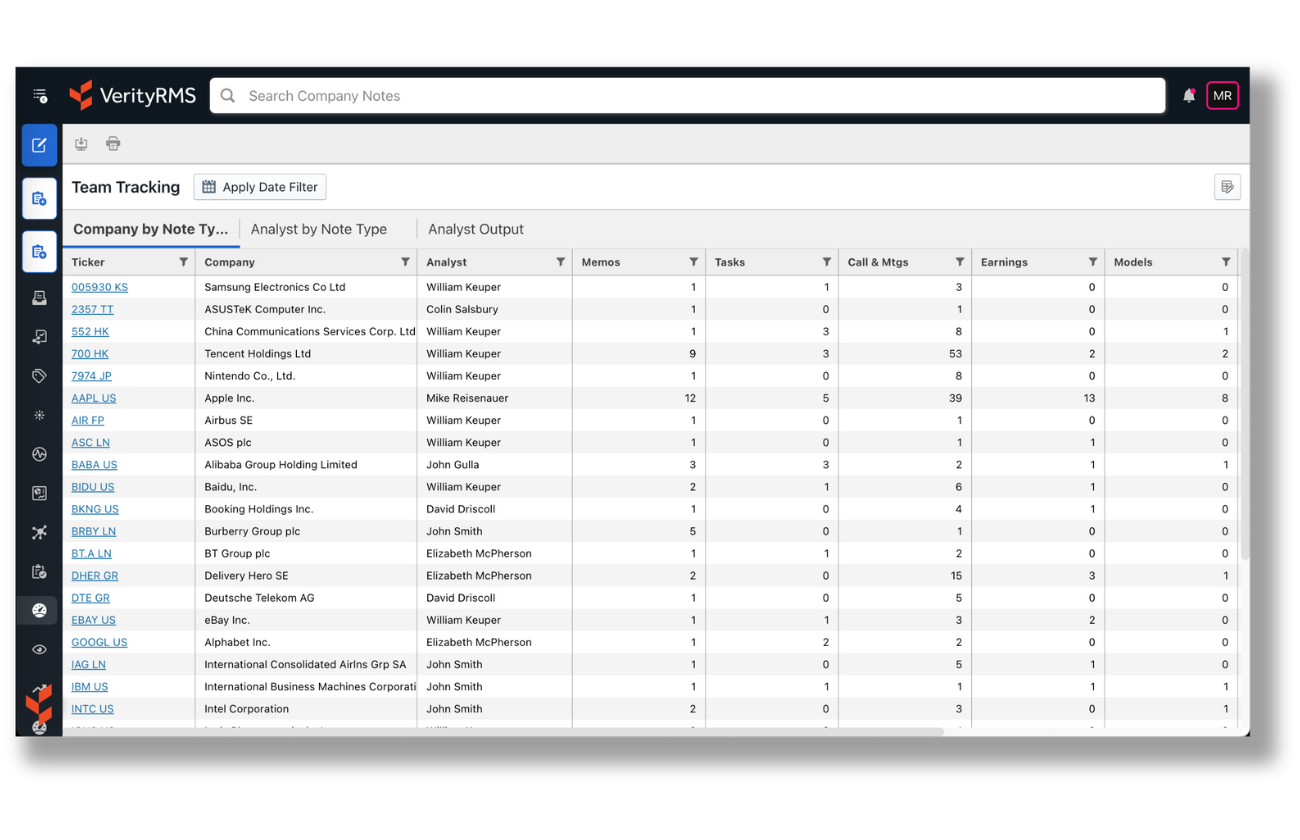

Stay on Top of the Team's Activity

Stay on top of your firm's data. Stay in tune with your team's progress, recommendations, price targets, models, activity, and more.

Features

-

Team tracking visualizes research activities.

-

System tracking lets compliance identify potential issues.

Sample idea pipeline dashboard

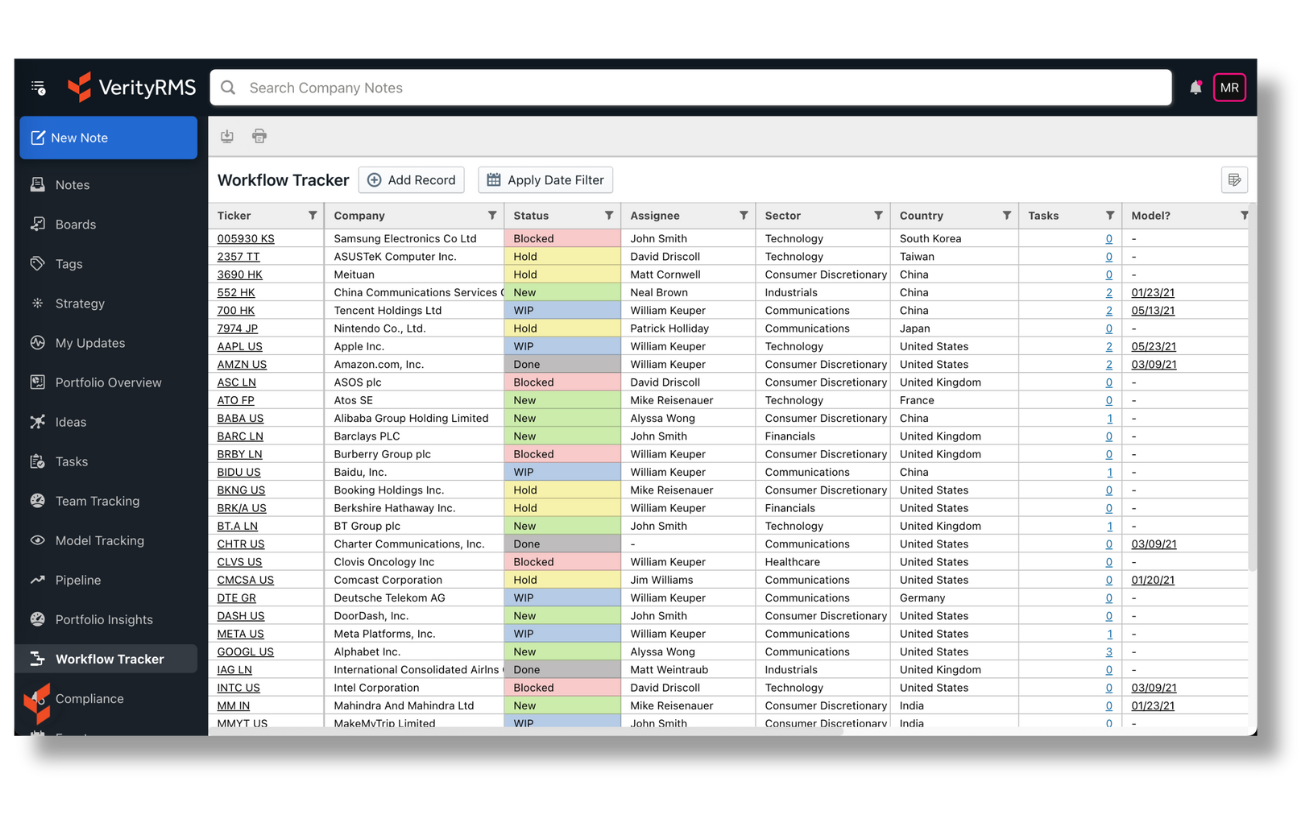

Sample workflow dashboard

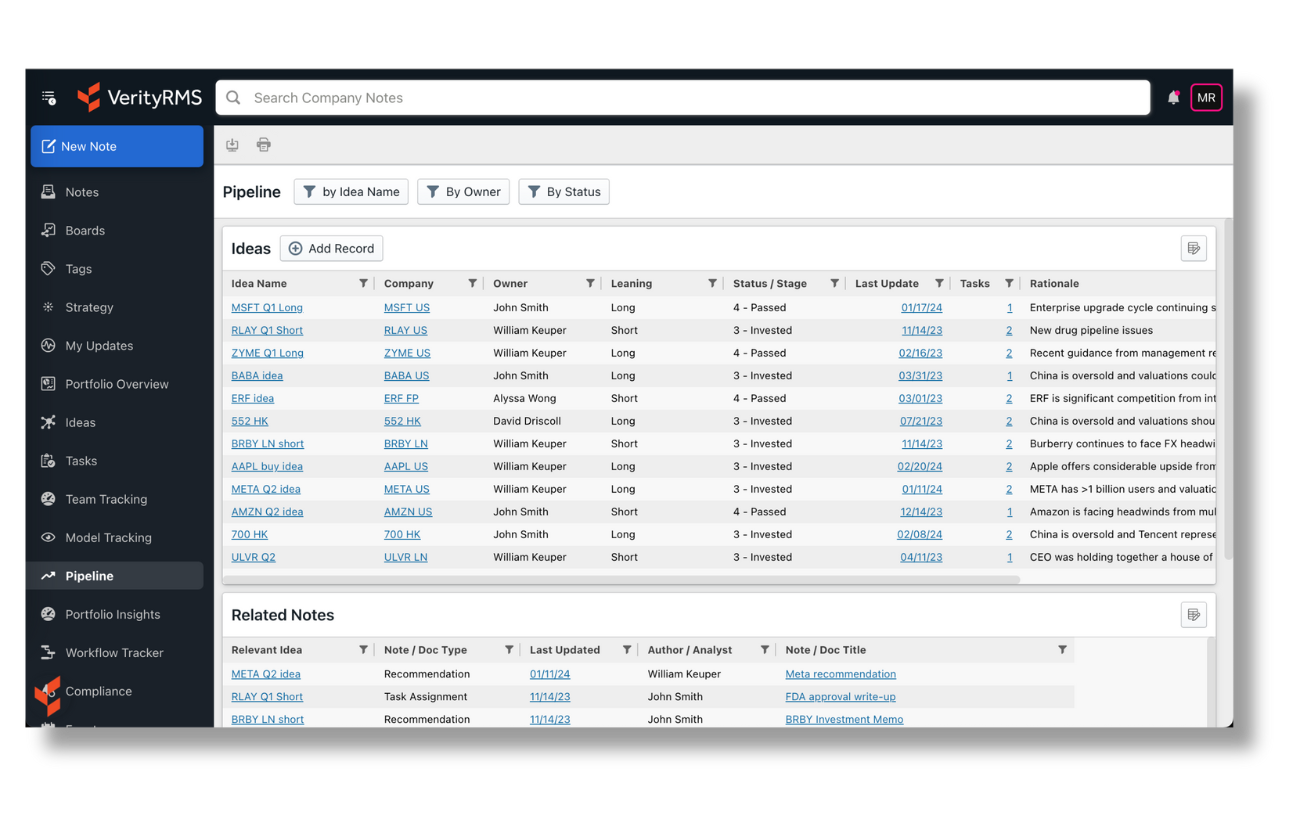

Speed Processes & Workflows

Reduce lag time. Avoid missed opportunities. Put your process into practice.

Features

-

Alerts & notifications make progress automatic.

-

Idea pipeline dashboards increase velocity.

Put GenAI to Work for Your Research Team

GenAI isn't going anywhere. Empower your talent with the ongoing AI innovations within VerityRMS.

Features

-

AI summaries give fast context.

-

AI extraction tools reduce time spent updating notes.

-

Integrates with VerityData GenAI Reports

VerityRMS

Your Process. Your Tools. One Integrated Workspace.

VerityRMS adapts to your process with stronger integrations than any other RMS provider.

Explore VerityRMS integrations

Experience the Power of VerityRMS Research Management System

See how Verity accelerates winning investment decisions for the world's leading asset managers.

Get My Demo